Blockchain technology has the potential to reduce costs, improve product offerings and increase speed for banks, according to the most recent report from the Euro Banking Association (EBA).

Founded in 1985 and supported by the European Commission, the EBA is a practitioner’s body for banks and other service providers that promotes a pan-European payment system and business practises.

Despite mostly dismissing digital currencies – the report notes they differ from “legitimate fiat currencies” – it asserts their applications are essential for “gaining more advanced knowledge of crypto technologies”.

These technologies are likely to be integrated with the existing financial system in the next one to three years, the EBA says.

“Apart from possibly being able to speed up processes and reduce their complexity, crypto technology applications in this area can also be integrated with legacy IT, legal frameworks and existing assets (currencies, stocks, bonds, etc).”

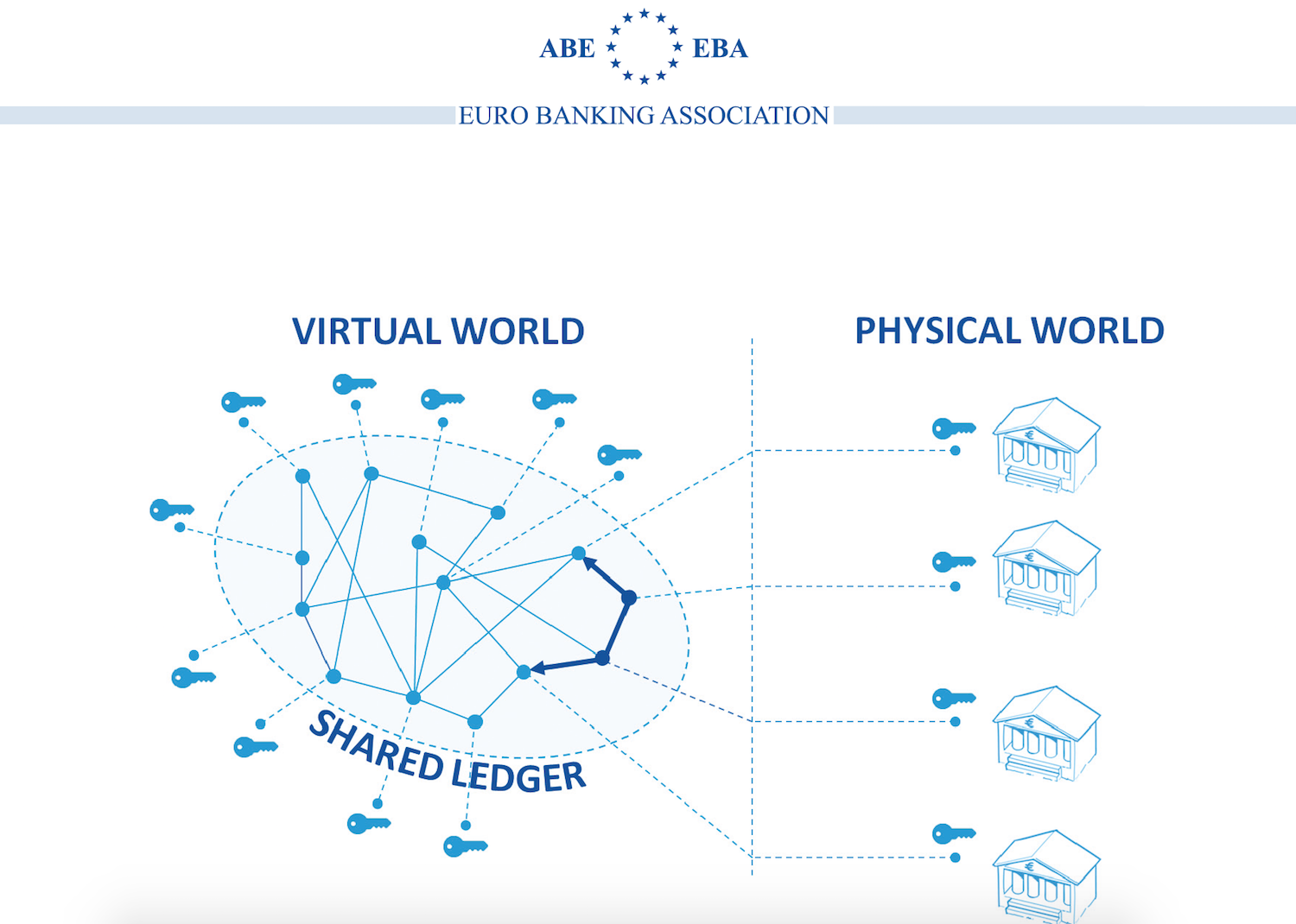

Crypto 2.0 and traditional banks

According to the EBA, cooperation, adoption and their two respective sub-drivers (communication and regulation) will be decisive factors in the future of the technology.

Here, the report says that the level of cooperation between Payment Service Providers (PSPs) and the crypto technology community – also between PSPs themselves – will determine the future relationship between banks and ‘crypto 2.0′ companies.

Notably, it draws parallels between the concerns and industry dynamics that surfaced when voice over Internet protocol (VoIP) applications such as Skype launched approximately ten years ago.

EBA’s report also speaks of two-fold benefits for PSPs and crypto businesses.

If regulation is favourable, PSPs may benefit from entering into partnerships with the crypto technology community, as they would be able to get a first-hand idea of long-term developments and would be better positioned to take advantage of the latter when the technology reaches the desired level of maturity.

In turn, it notes how the crypto technology community would benefit from the PSPs’ legitimacy and procedural knowledge, concluding:

“What can be safely said at this point in time is that crypto technologies are an area to be closely monitored and revised for further analysis.”

Though it is difficult to predict the way in which crypto technologies will the existing financial infrastructure, the report adds that further developments – and progress – can be expected.

Four use-case scenarios

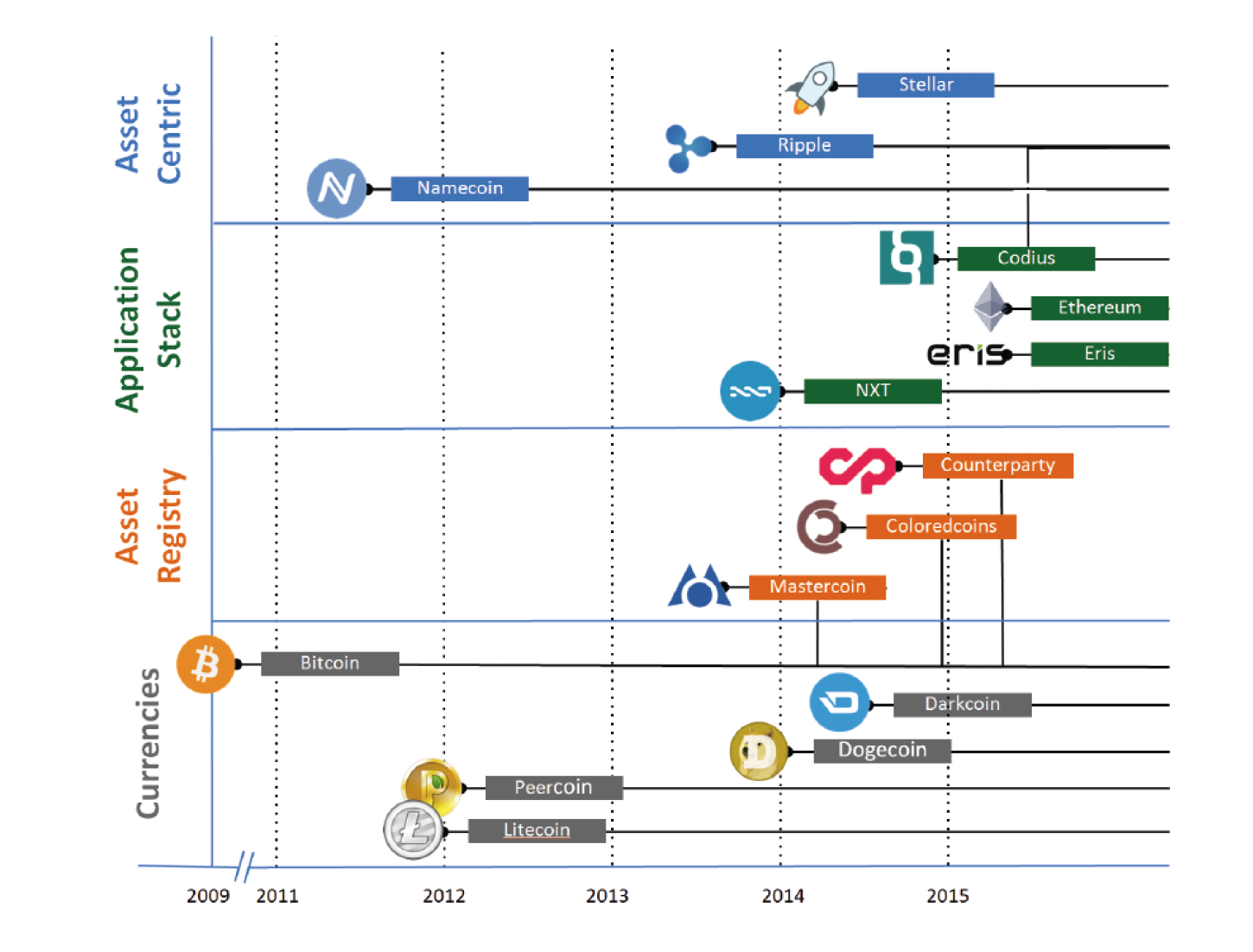

The report groups blockchain technologies into four key categories: currencies, asset registries, application stacks and asset-centric technologies. It notes, however, that the lack of regulatory and technical maturity diminishes the use-case for the first three, adding that they still warrant close monitoring by industry players.

A chronological representation of the four development categories of crypto technologies, according to EBA’s report.With this in mind, the paper describes four real use cases where blockchain technology could improve foreign exchange and remittances, real-time payouts, documentary trade and asset servicing – concluding that asset-centric developments were potentially the most interesting for transaction banking and the payments industry.

Progress in the other three areas has been hindered by technological and regulatory challenges, the EBA says.

The paper suggests that the banking and payment industries should attempt to “reach, conversion and cost advantages of currencies and reductions in auditing and governance expenditures from asset-centric as well as radical innovation from application stack technologies”.

Transformative potential

The EBA’s report follows on from a European Central Bank publication, which described digital currencies as “inherently unstable” but potentially transformative in the realm of payments.

Prominent bankers, such Santander’s Mariano Belinky and Barclay’s Usama Fayyad have commented on the ledger’s transformative potential and Swiss investment bank UBS recently opened a blockchain technology research lab in London to see how it could be applied in the wider FinTech community.

The blockchain has also captured the attention of companies from outside the banking space. US insurance giant USSA is allegedly pouring resources into investigating how to incorporate the blockchain into its existing infrastructure.

Author: Yessi Bello Perez